Key Takeaways:

- Demand exceeds supply: Buyers are actively hunting off-market deals, signaling a market under pressure.

- Scarcity drives performance: With no new construction, townhouse inventory remains structurally capped, boosting long-term value.

- Townhouses vs. condos: Since 2018, townhouses have outpaced condos in both price growth (+27% vs. +1%) and resilience through market shocks.

Receive the Private Edition

A version of this article appeared in the Private Edition newsletter. Sign up to receive future editions straight to your inbox.

The Manhattan Townhouse Market 2025

Over the past two months, I’ve received five inquiries about off-market townhouses in Downtown — a signal that the Manhattan townhouse market 2025 is under serious pressure. These weren’t casual buyers; they had already searched through every active listing and still found nothing.

Despite the attention that glass towers draw, it’s the townhouse—rare, resilient, and seemingly unlikely—that remains a highly sought-after asset class.

Townhouses make up a small part of New York housing. Few are ever built, and the city mainly focuses on new condo projects. Even when new townhouses do appear, they are often part of condo developments, arranged as condominiums with monthly fees and shared amenities instead of true single-family ownership. Examples include the five townhouses at Greenwich Lane in the West Village and the two townhouses at 20 East End in the Upper East Side.

Yet the figures are hard to ignore: except for 2017 and 2020, townhouse sales have consistently outperformed, while condos spent years underperforming, leading up to the pandemic.

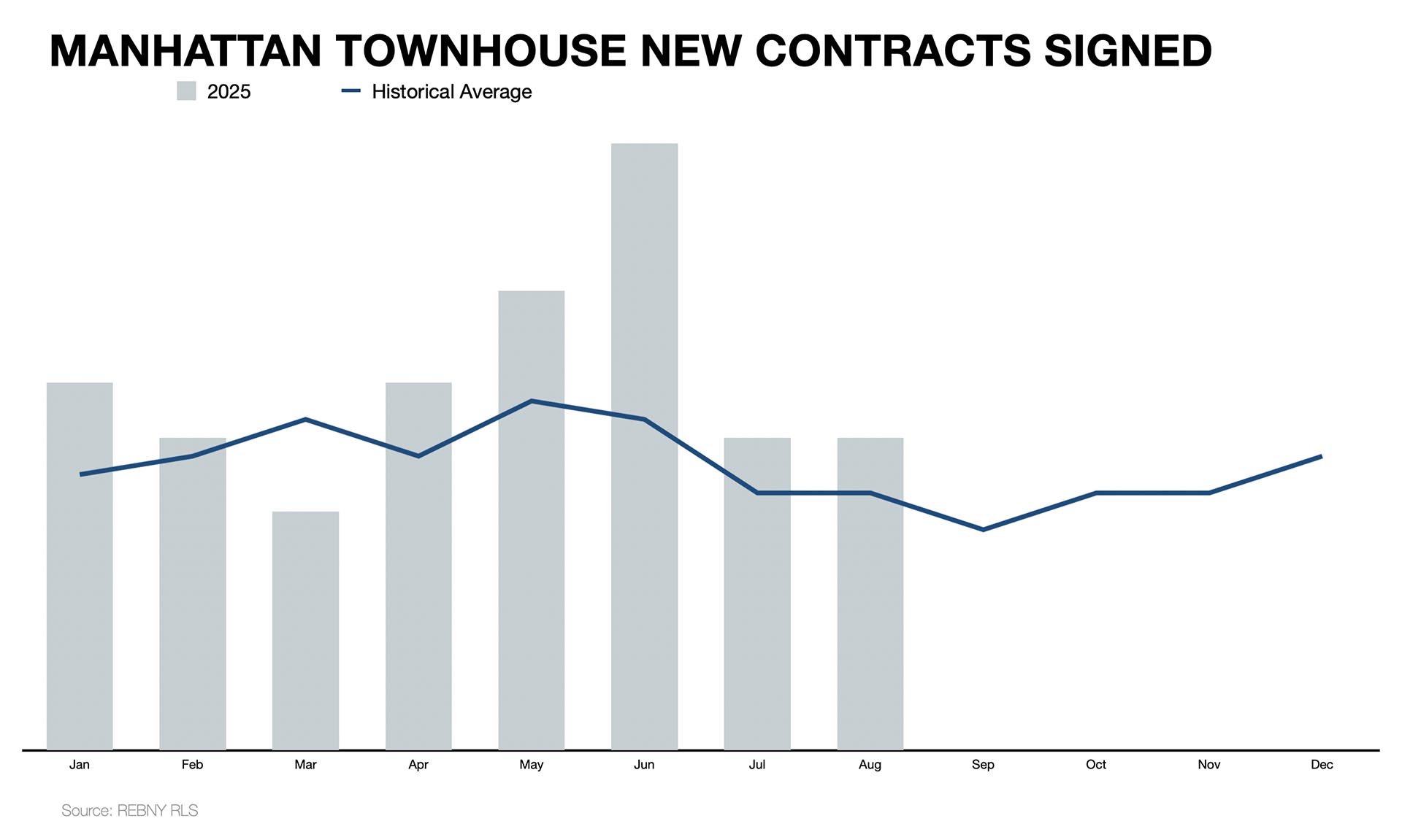

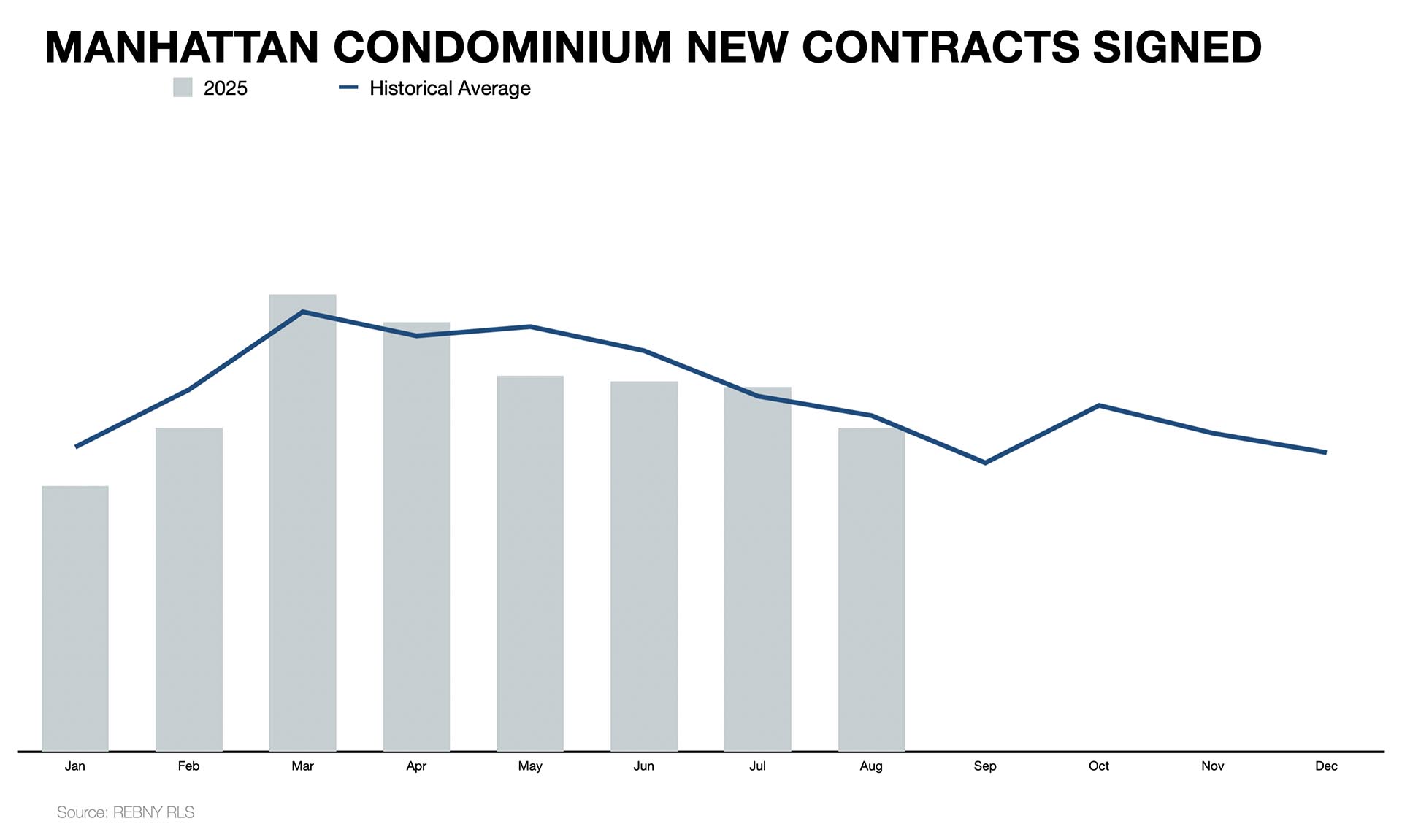

In 2025, seven of the past eight months have surpassed the historical average of contracts signed. Year-to-date, Manhattan townhouses are averaging 20 contracts a month, compared to a long-term average of 16. Condos, however, are underperforming compared to their historical baseline.

The supply side explains the difference. Unlike condos, townhouses aren’t developed through new projects. There’s limited land available for large-scale construction. When developers do participate, their focus is on purchasing existing properties for renovation or combining two side-by-side homes into one larger residence. It’s not about growing the market but repositioning what already exists.

That scarcity drives townhouse performance. Condos, by contrast, compete amid a steady stream of new supply. In 2025, the condo market averaged 393 contracts per month, below its historical baseline of 410.

The strength of the townhouse market is centered in two areas of Manhattan: Downtown—particularly the West Village and Greenwich Village—and the Upper East Side. These neighborhoods are mainly residential, marked less by skylines and more by tree-lined streets, local businesses, and neighborhood character.

For much of the 19th century, Manhattan’s wealthy residents lived in townhouses and private mansions. Apartments were considered dwellings for the working class, and even when developers marketed early multi-family buildings as “French flats,” the upper class resisted.

The shift began in the early 20th century. Rising costs of household staff and upkeep made large homes less practical, while the passenger elevator made vertical living both convenient and respectable. Developers capitalized on this change. Fifth Avenue mansions were torn down and replaced with luxury co-ops offering privacy and prestige without the burden of maintaining a full household staff.

One building in particular proved the concept: 998 Fifth Avenue, completed in 1912. Designed as a cooperative with spacious layouts and high-end finishes, it drew families who had previously sworn they would never live in an apartment. Its success confirmed the model, and by the 1920s, the co-op had become Manhattan’s dominant form of luxury housing until condominiums emerged.

The result is today’s structural limit. Unlike condos, which are replenished in each new development cycle, Manhattan’s townhouse stock was never rebuilt after that shift.

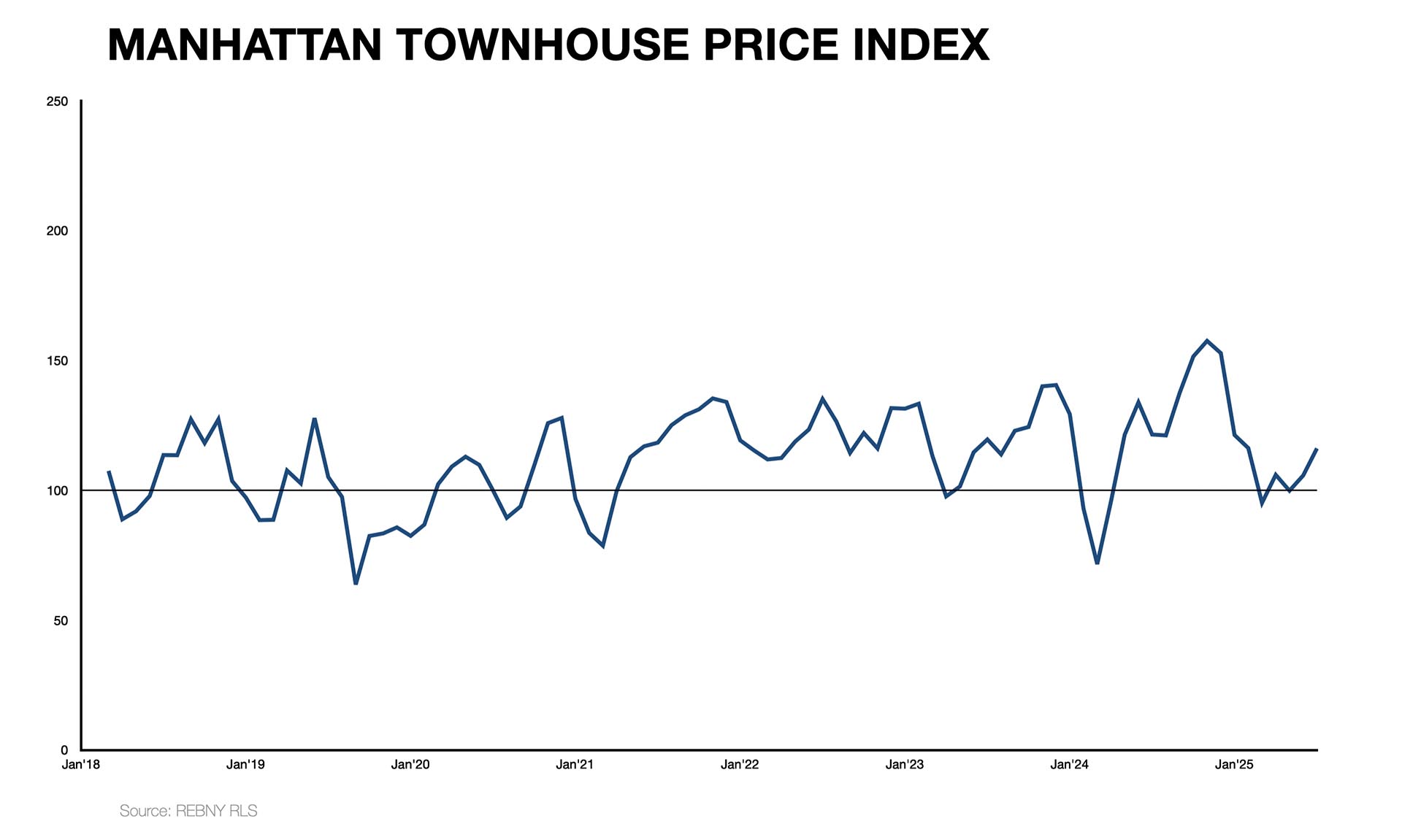

Prices in the townhouse market reflect this scarcity in real time. Throughout most of 2024, inventory levels remained around 14 months, leading to a slowdown in prices by September and October. However, since closings typically occur 45 to 90 days after contracts are signed, the index now shows that momentum is shifting upward again as supply has become tighter.

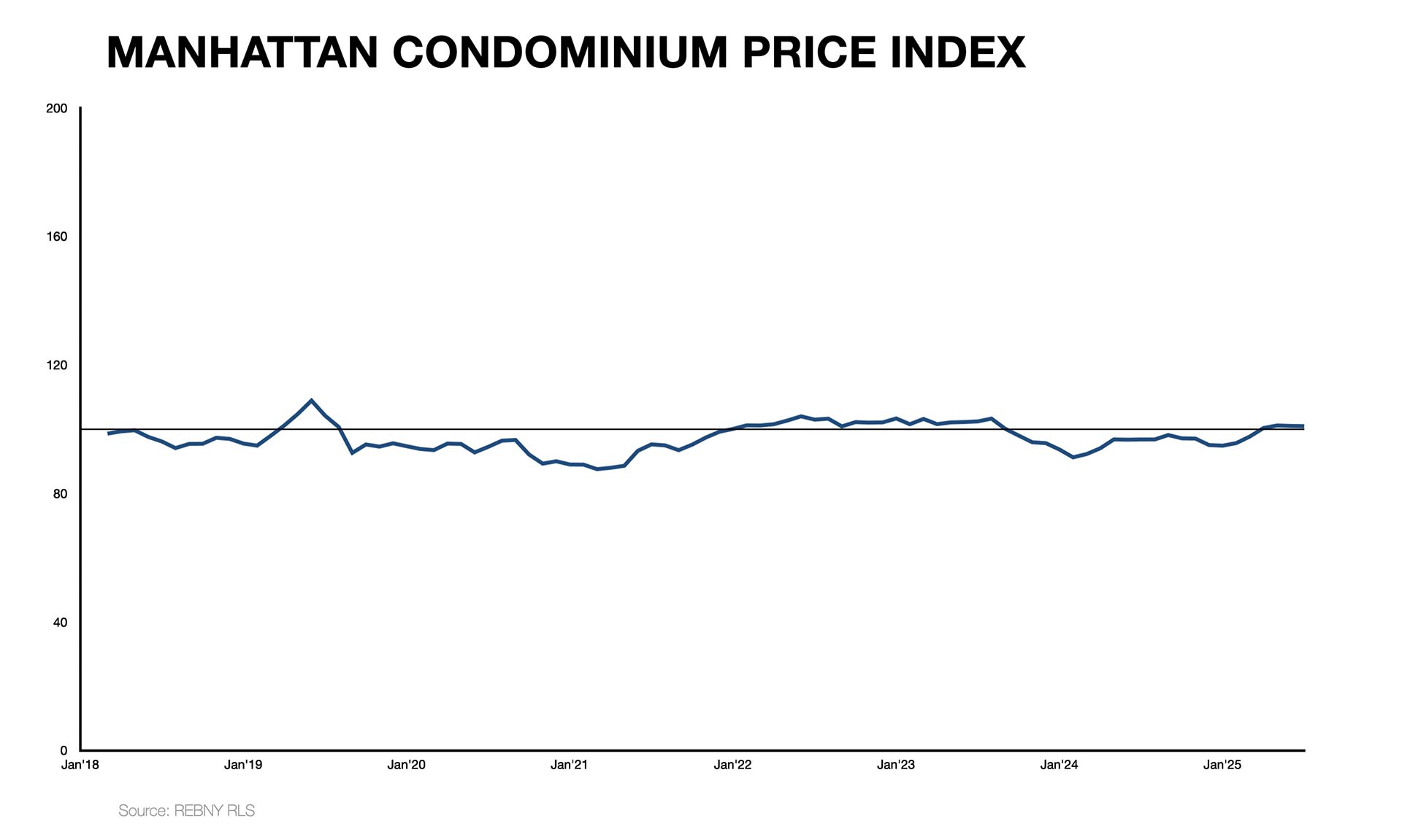

Since 2018, townhouse prices have increased much faster than condo prices. Compared to the Q4 2017 baseline, townhouses rose by 27% by July 2025, while condos only increased by 1%. In the luxury market, townhouses priced over $12 million experienced a 75% surge, compared to a 10% gain for condos priced over $5 million. Although townhouses are more volatile month to month, they have maintained their value better over time, remaining more resilient to market shocks like the mansion tax hike and the COVID-19 pandemic. As a result, townhouses have spent significantly more months above the baseline.

Taken together, the indices support the story: condos may lead in volume, but it’s townhouses—both in the overall market and in the ultra-luxury segment—that have proven to be the better long-term store of value.

At the very high end of the market, roughly the top 10% of sales, strength has been clear. Year-to-date, luxury townhouses are averaging three contracts per month, compared to a historical average of two. Demand is strongest on the Upper East Side and Downtown. Inventory is often elevated in this tier, but Downtown has slipped into seller’s territory with just 20 months of supply—a rare signal of strength in a segment that almost always favors buyers.

September is traditionally the month when inventory rises, as sales activity across the city heats up until the holiday season. How the townhouse market closes this year remains uncertain. However, if the first eight months are any indication, 2025 is already turning out to be a pivotal year for Manhattan townhouses.